Helping you buy with Help To Buy

If you have been searching for a new home, whether that new home is a real possibility or a distant daydream, the chances are that you will have seen the Help To Buy logo pop up on listings and adverts.

It’s easy to assume that such schemes won’t apply to you or to get confused by the financial jargon, but the Help To Buy scheme is easy to understand and applicable to more people and houses than you would initially think. However, with the deadline for Help To Buy ISAs already passed and changes to the Help to Buy Equity Loan scheme (restricting it to first-time buyer and including a regional property price cap) taking place in April 2021, the clock is ticking!

Who can take advantage?

Currently, the Help To Buy Equity Loan scheme is open to everyone (not just first time buyers) who wishes to buy a new home (provided that home is newly built), on houses up to the value of £600,000. It is due to run up to April 2021, but it may close earlier if all the funding is taken up before then.

How does it work?

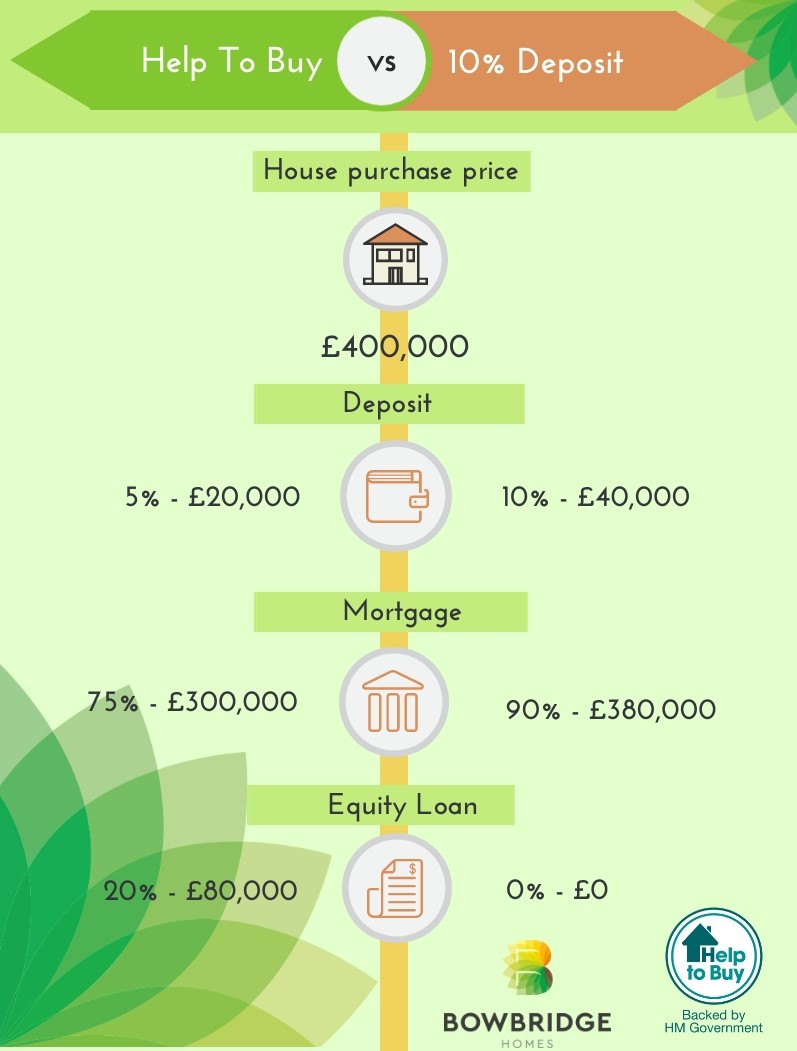

The scheme works by offering house buyers the opportunity to buy 100% of their home with only a 5% deposit and a mortgage to the value of 75% of the house’s value. The remaining 20% comes from a government backed equity loan. This opens up much more competitive mortgage rates, as you will have a much lower LTV (Loan To Value). In London, a 5% deposit is still required but a 40% equity loan is available.

Essentially, most people buying a home put down a 10% deposit which means that their mortgage is 90% and so their LTV is 90%. Buyers using the Help To Buy Scheme will only have a mortgage (and therefore an LTV) that is 75%. House buyers with a higher LTV are of greater risk to the lenders and so therefore mortgage interest rates are higher. In contrast, a lower LTV results in lower interest rates.

This, teamed with only having to save a 5% deposit rather than the seemingly impossible for many 10% deposit, makes Help To Buy an extremely attractive proposition for many house buyers.

What else do you need to know?

With all schemes like this, it is important for you to know exactly what you’re signing up for. Here are some things to be aware of with the Help To Buy scheme;

- The equity loan is interest free for the first five years (bar a £1 monthly management fee). However, after five years, in addition to the management fee, the equity loan is subject to interest at 1.75% per annum on any outstanding amount and this rises annually by RPI inflation. The interest will only be chargeable on the original amount borrowed.

- The home purchased through Help To Buy must be your main residence, must not be rented out and must not be a second home.

- The loan must be repaid after 25 years. You can repay part or all of the loan early, but you can only pay a minimum of 10% of the property’s current value at any one time.

- If you sell your house and the equity loan has not been repaid, the government will take a percentage of the total sale price. For example, if 10% of the equity loan is still outstanding and you sell your house for £300,000, the government will be entitled to £30,000 to repay the loan.

Help To Buy with Bowbridge Homes

At the time of writing, all our homes currently on the market at both The Stables in North Kilworth and Northdale Park in Raunds are eligible for the Help To Buy scheme. Therefore, you can take this opportunity to get on the property ladder, get some more space for your growing family or move to that location you never thought you would be able to afford!

Still confused? Contact our sole sales agent, Connells, for more information (Northdale Park in Raunds – 01933 808 946, The Stables in North Kilworth – 01858 465 921)